Westpac is one of New Zealand’s largest and most trusted banks, offering a wide range of home loan products. Whether you’re a first-time homebuyer, looking to refinance, or want to upgrade your property, Westpac provides various mortgage options with competitive home loan rates.

In this guide, we will cover the current Westpac home loan rates, types of loans they offer, and the factors that influence these rates.

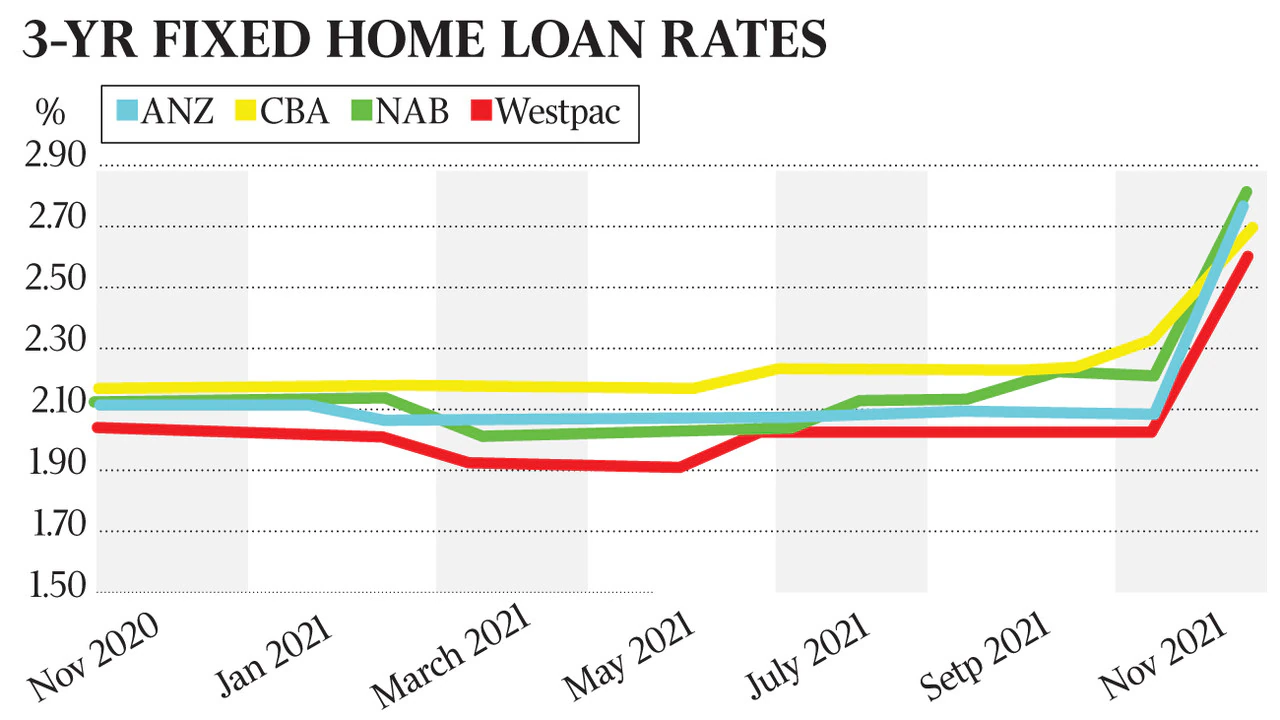

1. Current Westpac Home Loan Rates

Westpac offers both fixed-rate and variable-rate home loans, along with combinations of both for flexibility. Below is an overview of Westpac’s typical home loan rates:

| Loan Type | 1-Year Fixed Rate | 2-Year Fixed Rate | 3-Year Fixed Rate | 5-Year Fixed Rate | Variable Rate |

|---|---|---|---|---|---|

| Westpac Home Loan Rate | 6.40% | 6.60% | 6.70% | 6.80% | 6.25% |

Please note, these rates are indicative and may vary based on the applicant’s financial profile, the loan amount, and other criteria. Rates are also subject to change based on market conditions and Reserve Bank of New Zealand’s Official Cash Rate (OCR).

2. Types of Home Loans Offered by Westpac

Westpac offers a variety of home loan products to suit different borrowing needs. Each loan type comes with its own set of features, advantages, and interest rates.

Fixed-Rate Home Loans

A fixed-rate home loan allows you to lock in an interest rate for a specific period, ranging from 6 months to 5 years. This provides certainty in monthly repayments as the rate does not change during the term.

| Advantages | Disadvantages |

|---|---|

| Predictable monthly payments | Limited flexibility if rates drop |

| Protection from rising interest rates | Higher rates than variable loans |

| Suitable for budgeting and financial stability | Penalties for early repayment |

Variable-Rate Home Loans

A variable-rate loan has an interest rate that changes over time based on market conditions. This type of loan is ideal for those who are willing to take on some risk in exchange for potentially lower rates.

| Advantages | Disadvantages |

|---|---|

| Flexibility to make extra repayments without penalty | Monthly repayments may increase if rates rise |

| Often comes with lower starting interest rates | Uncertainty with changing repayment amounts |

| Can be refinanced easily if rates fall | Less predictability in monthly budgeting |

Split Home Loans

Westpac also offers split home loans, where you can divide your mortgage between fixed and variable rates. This gives you a balance of the stability of fixed rates and the flexibility of variable rates.

3. Factors Affecting Westpac Home Loan Rates

Several factors influence the interest rates on home loans at Westpac. These include:

1. The Reserve Bank of New Zealand’s OCR

The Official Cash Rate (OCR) set by the Reserve Bank of New Zealand directly impacts home loan rates. When the OCR rises, borrowing costs increase, which can lead to higher interest rates for home loans.

2. Loan-to-Value Ratio (LVR)

Westpac evaluates the Loan-to-Value Ratio (LVR) to determine the level of risk associated with a home loan. A higher LVR (where you borrow more relative to the value of the property) typically results in a higher interest rate due to the increased risk for the lender.

3. Your Credit Profile

Westpac, like most lenders, assesses your credit score to determine the interest rate you’ll be offered. Those with a higher credit score may qualify for lower rates, as they are seen as less risky to lend to.

4. Loan Term

The length of the loan term also plays a role in the interest rate. Shorter loan terms typically have lower rates as the lender’s risk is reduced, while longer loan terms may have slightly higher rates.

5. Economic Conditions

Interest rates fluctuate based on broader economic conditions such as inflation, unemployment, and economic growth. When the economy is strong, interest rates may rise, and when it’s weaker, they may fall.

4. How to Get the Best Westpac Home Loan Rate

Securing the best possible home loan rate from Westpac requires careful planning and understanding of what affects interest rates. Here are a few tips:

1. Improve Your Credit Score

A good credit score (typically above 700) can help you secure a lower interest rate. Paying bills on time and reducing debt can improve your credit score and increase your chances of getting the best rate.

2. Save for a Larger Deposit

The larger your deposit (down payment), the lower your LVR, which can help you secure a better interest rate. A deposit of at least 20% can prevent you from paying for Lenders Mortgage Insurance (LMI), which further lowers costs.

3. Consider Loan Terms

The loan term you choose can impact your home loan rate. Shorter terms often have lower rates, but higher monthly repayments. If you can afford higher payments, a shorter term could save you money in the long run.

4. Consider Refinancing

If interest rates drop or your financial situation improves, consider refinancing your Westpac home loan. This can help you take advantage of lower rates and reduce your overall loan costs.

5. Look for Special Offers

Westpac frequently offers special deals, including cashbacks or discounted rates for first-time homebuyers or those looking to refinance. Keep an eye on such promotions to get the best deal.

5. Westpac Home Loan Fees

While Westpac offers competitive home loan rates, there are additional fees to consider when applying for a mortgage. Some common fees include:

- Establishment Fee: A fee for setting up your home loan.

- Valuation Fee: A cost for assessing the value of the property you’re purchasing.

- Legal Fees: Costs associated with processing the loan and transferring ownership.

- Early Repayment Fee: Charges for repaying your loan early, particularly for fixed-rate loans.

- Monthly Service Fee: A fee for maintaining the loan on a monthly basis.

These fees should be factored into the overall cost of your loan to get a full understanding of your borrowing costs.

6. How to Apply for a Westpac Home Loan

Applying for a home loan with Westpac is straightforward. Here are the steps:

1. Pre-Approval

Start by applying for pre-approval with Westpac to get an idea of how much you can borrow. This step involves a credit check and financial assessment to determine your borrowing capacity.

2. Choose Your Loan Type

Choose between a fixed-rate, variable-rate, or split home loan depending on your preferences and financial situation.

3. Submit Required Documents

You will need to provide documents such as proof of income, bank statements, identification, and details of the property you intend to purchase.

4. Loan Assessment

Westpac will assess your application, including your financial situation, the property’s value, and your credit history.

5. Approval and Settlement

Once your loan is approved, you can proceed to sign the loan agreement and settle the loan. After settlement, your home loan will be in place, and you can begin making repayments.

Westpac provides competitive home loan rates and a variety of mortgage options to suit different financial situations. By understanding the current rates, loan types, and how factors like your credit score and LVR can impact your rates, you can secure a home loan that best fits your needs.